Information is the 21st Century gold, and financial institutions are aware of this. Armed with machine learning and artificial intelligence technologies, they have the opportunity to analyze data that originates beyond the bank office. Financial companies collect and store more and more user data in order to revise their strategies, improve user experience, prevent fraud, and mitigate risks. In this article, we will talk about how Artificial Intelligence and Machine Learning are used as well as the benefits and risks of these solutions.

Artificial Intelligence in Banking Statistics

- According to a forecast by the research company Autonomous Next, banks around the world will be able to reduce costs by 22% by 2030 through using artificial intelligence technologies. Savings could reach $1 trillion.

- Financial companies employ 60% of all professionals who have the skills to create AI systems.

- It is expected that face recognition technology will be used in the banking sector to prevent credit card fraud. Face recognition technology will increase its annual revenue growth rate by over 20% in 2020.

Benefits of Machine Learning in Banking

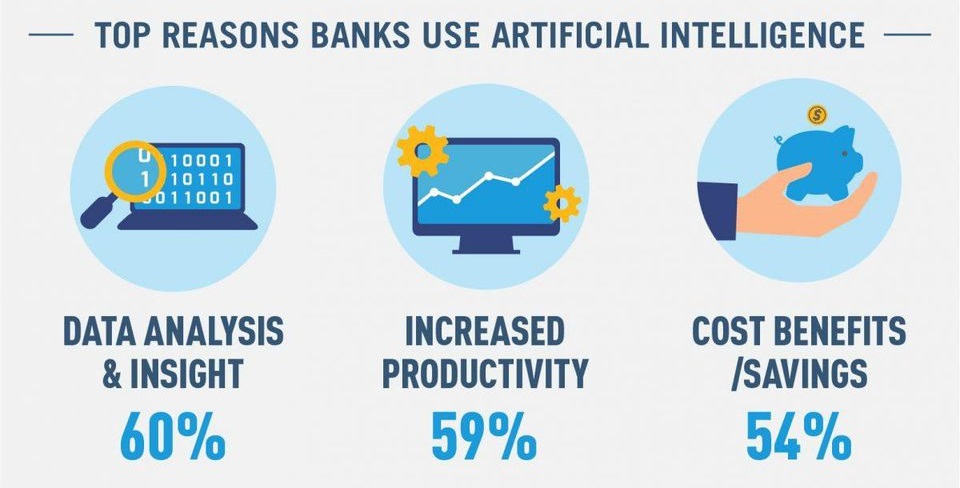

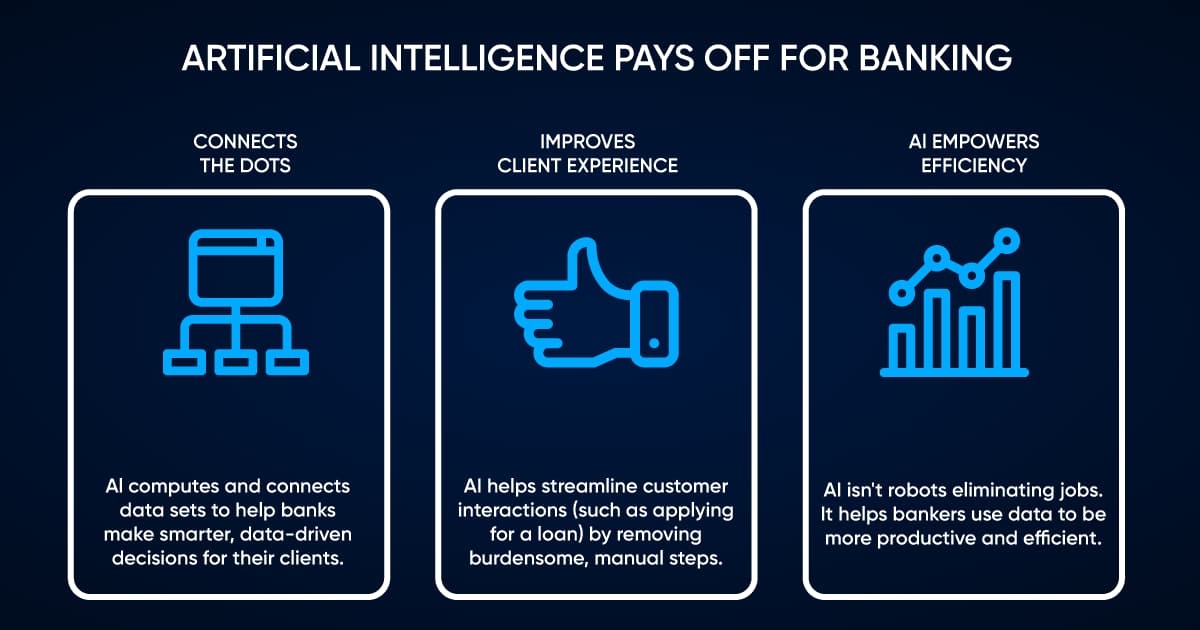

Artificial Intelligence and Machine Learning are able to provide unprecedented levels of automation, either by taking over the tasks of human experts, or by enhancing their performance while assisting them with routine, repetitive tasks. But what are the main benefits of Machine Learning in Banking? This question has many possible answers, and what is even more interesting, the number of answers will continue to expand as the newest technological solutions hit the market. Here is an attempt to highlight the most important ones:

Greater Automation and Improved Productivity

Artificial Intelligence and Machine Learning can easily handle mundane tasks, allowing managers more time to work on more sophisticated challenges than repetitive paperwork. Automation across the entire organization will ultimately lead to greater profits.

Personalized Customer Service

Automated solutions with Big Data capabilities can track and store as much information about the bank’s customers as needed, providing the most precise and personalized customer experience. Optimizing the customer footprint allows banks to leverage analytical capabilities of Artificial Intelligence and Machine Learning to detect even the most subtle tendencies in customer behavior, which helps create a more personalized experience for each individual client. We discussed this topic in great detail in the Customer Behavior Analysis with Artificial Intelligence article.

More precise Risk Assessment

Having an accurate digital footprint of each customer also can help banks reduce uncertainty for managers working with individual clients. The automated system is more accurate than a human in such areas as analysis of loan underwriting, eliminating any possible human bias.

Advanced Fraud Detection and Prevention

This is probably the top benefit of AI/ML for any financial institution because there has historically been, and will continue to be, criminals who are devising methods to commit financial fraud. Fortunately, there are currently a wide range of proven methods and techniques of ML-powered Fraud Detection on the market. We will talk about all of them in greater detail in this article, and you will find out how to make your bank even more secure thanks to these technological innovations!

Don't have time to read?

Book a free meeting with our experts to discover how we can help you.

Book a MeetingFraud Prevention in the Banking Industry: Fraud Statistics 2019

In 2019, malicious digital attacks hit users here and there — leading to massive data breaches and the leakage of vulnerable information. That’s not a case to ignore for Banking industry owners and payment service providers who are highly concerned about their customers’ loyalty and safety. According to the statistics of the U.S. Federal Trade Commission, fraud reports in 2019 included more than 388,588 cases that resulted in $1.9 billion of losses. More detailed loss statistics of payment method fraud is displayed in the table below:

| Fraud type | # of reports | Losses |

|---|---|---|

| Wire Transfers | 73,542 | $439M |

| Credit Cards | 53,763 | $135M |

| Gift/Reload Cards | 38,401 | $103M |

| Bank Account Debit | 35,436 | $89M |

| Internet/Mobile | 25,055 | $84M |

| Cash/Cash Advance | 12,411 | $120M |

| Check | 7,246 | $72M |

| Money Order | 3,868 | $23M |

| Telephone Bill | 956 | $2M |

How Artificial Intelligence is Used for Fraud Monitoring in Banks

The data that banks receive from their customers, investors, partners, and contractors is dynamic and can be used for different purposes, depending on which parameters are used to analyze them. Basically, the scope of AI for banking can be grouped into five large groups.

Improving Customer Experience

When banks and other financial organizations got the opportunity to learn everything about a user and his behavior on a network, they simultaneously gained the opportunity to improve the user experience as much as possible.

Chatbots

For example, if a user has difficulty working with a website or application, chatbots are used to lead him along the right path and at the same time reduce bank support staff’s workload. In addition, modern chatbots can perform simple operations such as locking and unlocking cards as well as send notifications to the user if he has exceeded the overdraft limit — or vice versa if the account balance is higher than usual.

Personalized Offers

Having a variety of information about user behavior allows financial companies to find out what customers want at the moment, and moreover what they are willing and able to pay for. So, for example, if a client was looking at ads from car dealers, then it might make sense to develop a personalized loan offer — of course, after analyzing his solvency and all possible risks.

Customer Retention

Modern AI systems working with big data in banking can not only analyze, but also can make assumptions. For example, in a number of cases, it is possible to predict the intentions of the client if he wants to refuse the services of a banking organization. The knowledge of this intention signals that it is necessary to take additional retention measures, create even more targeted and personalized offers, and as a result, improve the customer experience.

Banking Fraud Detection

Banking Fraud Detection is in the first place linked to the detection and prevention of damaging operations that deal with transaction failures, returns, disputes, and money laundering, among others. A much safer strategy for every payment service is to set a reliable fraud prevention system rather than deal with the consequences of bad customer experiences and fraud losses.

Is Machine Learning Efficient for Bank Fraud Detection?

How do banks detect fraud?

The process of revealing a fraudulent transaction is not as easy as a bank customer might think. Even if the victim realized her bank account was corrupted, there’s still a checklist that she must go through before the bank or service provider opens a fraud investigation, such as providing any details or evidence that the fraud took place. However, the customer’s liability in the case of debit or credit card fraud is different — that’s why any victim should inform the bank as quickly as possible for debit card fraud as any delay will result in liability of up to $500.

If the bank received proof that fraud really took place, it will have to investigate the case within 90 days at the most. The customer is further recommended to ask the credit reporting agencies to place a note on their files to forbid the creation of new credit contracts with their identity unless they physically appear into the bank to submit them.

How can banks reduce fraud?

Banks and payment service providers might be equipped with a bunch of rule-based security measures to detect fraudulent activities in users’ accounts. However, these systems — if not based on Machine Learning for fraud prevention — are quite primitive and inflexible. For example, making a customer enter their password every time they submit an order to ensure there will not be a possibility of fraud.

In the case of AI-driven fraud prevention, we are talking about several levels of threat that the transaction might have. If the threat level is higher than a certain pre-established threshold, depending on the location, the user’s device, etc. the algorithm will demand an additional identity check such a via a text message or a phone call.

Fraud detection software for banks

The Internet is full of advertisements about solutions that promise to prevent fraud for a reasonable cost. They claim to build fraud prevention logic around anomaly detection or predictive or descriptive analytics. At the end of the day, they still have to try and find the best and most competitive solution to stand out among them all. Therefore, let’s look into three vendors who offer fraud detection software for banks.

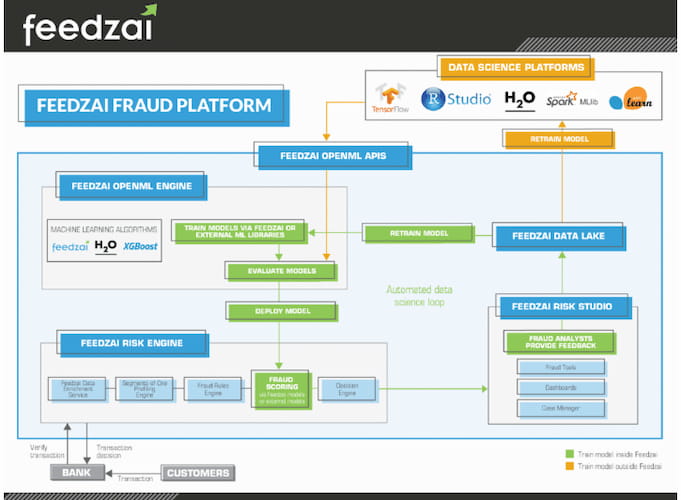

Feedzai

Feedzai is a company that offers bank fraud and money laundering prevention solutions, using the anomaly detection technique at its core.

Their OpenML Engine software is designed for use by data engineers from the client’s side, so they can build custom Machine Learning models.

Data Visor

Data Visor is one of the solutions that work on a predictive analytics basis and specializes mostly in individual loan risk rating. The software provider claims to support fraud monitoring in several client’s loan applications simultaneously. They promise to uncover even the most subtle fraud correlations in transactions with unsupervised Machine Learning methods.

Teradata

Teradata offers software for fraud monitoring in banks that has an AI model at its core and is able to actively learn on new data about transactions. It helps the user by notifying him about possible fraud while maintaining the function to mark falsely fraudulent transactions so that the model could improve on them.

Advantages of AI fraud monitoring in Banks

From the previous section, we already know that fraud prevention solutions can be built on an old rule-based approach, which is now uncommon, or prescriptive/predictive analytics based on Machine Learning and anomaly detection in particular. So, what is it about AI that makes bank fraud detection and prevention more effective than other methods?

Unlike purely rule-based software, AI-based solutions can smartly derive correlations in fraudulent activity to further detect new fraudulent patterns. Simply writing rules can’t cover the whole diversity of scenarios that can let a fraudster’s transaction be unnoticed among others; moreover, it is hard to make these rules accurate enough.

Some signs that can give the model a hint on how to tell a good transaction from an illegal one are the following: customer behavior (how he usually makes purchases, his usual location, etc.); aggregated data analysis; and control of user ID information.

Types of Bank Fraud

As stated by the Consumer Network Sentinel Data Book 2019, the most serious threat for banks is credit or debit card fraud. The median loss for a person out of the yearly fraud losses ($224M) is around $320, while statistics show that younger people are more exposed to fraud than people ages 30 and older. The most concerning thing about this report is that only 23% of people reported their losses, meaning that most fraudsters’ illegal affairs remain in the dark while the victim keeps losing money.

How much do banks lose to fraud?

Among the types of fraud that are specifically a threat to the Banking industry are credit or debit card fraud, employment or tax-related fraud, mortgage fraud, and government document fraud. Let’s take a closer look at each of these types.

| Fraud type | Reports 2019 (#) | Amount loss |

|---|---|---|

| Credit or Debit Card Fraud | 53,763 | $224M |

| Employment or Tax-Related Fraud | 45,564 | $110M |

| Government Document Fraud | 12,474 | $12M |

| Mortgage Foreclosure Relief and Debt Management Fraud | 10,605 | $0.6M |

Credit or Debit Card Fraud

Credit or debit card fraud has been topping the list of types of bank fraud for a long time. It is that popular because there are numerous ways to secretly get your credit card information. Once access to the card is available, the robber can start using your money, while most other bank fraud types are more sophisticated to perform. Sources from where the robber gets the information are as varied as discarded receipts, credit card statements, any documents containing your bank account number, credit card skimmers on ATMs, etc.

Credit card fraud is usually detected with Machine Learning methods such as supervised or unsupervised anomaly detection and classification or regression techniques. To train a robust Machine Learning model to detect card fraud, the most important aspect is a large and representative set of fraudulent and good transactions combined with a feature extraction phase performed by a skillful data analyst.

Mortgage Fraud

Mortgage fraud for profit implies, first of all, altering information about the loan taker. Institutions such as banks, credit unions, and other financial institutions are exposed to the threat of mortgage fraud.

The fraudster usually provides false information about the loan taker’s income to borrow a larger sum of money. Machine Learning for fraud detection can score bad borrowers based on the history of their transactions and find suspicious information in their documents in order to pass the case to a bank professional for deeper validation.

You can learn about some of the latest types of mortgage fraud by visiting the official FBI website.

Document Forgery/Counterfeiting

Document forgery or counterfeiting is the type of fraud often referred to as identity theft. Fraudsters can forge, counterfeit, or steal a victim’s documents to use online for taking a loan or obtaining other illegal favors. Information on the document can be changed entirely or partially, depending on the criminal’s goal. Examples of such changes include the date or place of birth, home address, fake watermarks/stamps, and adding pages from another document to the current one.

One of the top places to buy documents illegally is the so-called black market. Criminals tend to use an illegally obtained ID with someone else’s photo or personal details to fool the system. If the system does not have a strong enough identity validation system to spot forgery and illegal activity, or does not have one at all, it becomes very vulnerable to possible fraud attacks.

Machine Learning has many algorithms that work with images and can classify them as fraudulent or not by finding out specific features and correlations. For example, if we need to spot a fake watermark on the document with an algorithm, we should first train a model on a specific amount of fake and genuine documents so that it will easily discover a counterfeit one. The same rule applies to blurry digits or uneven lines that might be the result of an image- altering program such as Photoshop.

Additionally, there are some anti-spoofing methods that we can use to understand whether a document is a printed copy or the original.

Machine Learning for Safe Bank Transactions

The main advantage of machine learning for the financial sector in the context of fraud prevention is that systems are constantly learning. In other words, the same fraudulent idea will not work twice. This works great for credit card fraud detection in the banking industry.

How Artificial Intelligence Makes Banking Safe

Most financial transactions are made when the user pays for purchases on the Internet or at brick-and-mortar businesses. This means that most fraudulent transactions also occur under the pretext of buying something. AI in banking provides an opportunity to prevent this from happening. For example:

- Cameras with face recognition can determine whether a credit card is in the hands of the rightful owner when buying at a physical point of sale.

- Tracking suspicious IP addresses from which a financial transaction occurs may help prevent fraud with discount coupons as well as identify fraudulent intentions. For example, if someone buys a product in order to return a fake one in its place.

Market Research and Prediction

Machine learning in conjunction with big data can not only collect information but also find specific patterns. For example, it is possible to foresee currency fluctuations, determine the most profitable ideas for investing, level credit risks (and also find a middle ground between the lowest risks and the most suitable loan for a specific user), study competitors, and identify security weaknesses.

Cost Reduction

Machine Learning allows financial organizations to identify weaknesses in processes and organize the work of full-time employees more efficiently. The simplest example is chatbots, which can successfully cope with advising clients on simple and standard issues. Chatbots also don’t require payment for their work! Besides the fact that working with ML allows companies to reduce costs, it is logical that it also helps increase profits due to improved customer service.

Machine Learning for Bank Transactions Monitoring

While some groundbreaking technologies do not meet their high expectations, when we talk about Machine Learning in the context of monitoring electronic payment transactions, it is the obvious solution for the future. Setting appropriate threshold levels for alerts in traditional monitoring systems has been a common problem for years. When the threshold is too low, you will end up with a big number of alerts, all of which require further investigation. When the threshold is too high, you may end up missing suspicious transactions altogether. The quick removal of false positives is another issue that should be addressed. The timely removal of false positives could be a major source of improvement in the effectiveness of the whole monitoring system. Humans can only handle the aforementioned tasks to a certain degree.

Transaction monitoring is one of the most beneficial applications of Machine Learning in the banking sector. ML-powered Predictive Analytics platforms have already made an impact in many industries, and finding anomalies in transactions is definitely one of them. If you are looking for a way to fortify your decision support system, ML can offer an entirely new level of automated analysis, either by replacing or assisting your experts in improving both security aspects and operational efficiency.

DO YOU WANT TO KNOW HOW TO USE AI AND MACHINE LEARNING IN FRAUD DETECTION?

Read this article to get all the details on this topic!

AI/ML in Fraud DetectionMachine Learning Use-Cases in American Banks

Artificial Intelligence is more than just a buzzword in the world of Banking and Finance. AI and ML solutions are already helping banks all over the world turn data into profit by providing a safer and more convenient environment for businesses.

The number of Machine Learning use cases in worldwide banking are constantly growing. It’s not surprising, because automated customer support, real-time Fraud Detection, better customer data management, risk modeling, and marketing strategy planning are the benefits that every bank can use to improve its processes. In this article, we will focus on the most prominent use cases of Artificial Intelligence and Machine Learning in the Banking industry in the United States. However, there are plenty of other notable cases we encourage you to discover from all over the globe. Focusing on the American banks that we will highlight right now, it is up to you to decide whether Artificial Intelligence and Machine Learning are trends, of the future, or if they are already the new technological standard that every organization should implement as soon as possible.

This leading bank in the United States has developed a smart contract system called Contract Intelligence (COiN). The algorithm based on data and machine learning helps quickly find necessary documents and important information contained in them. At the moment, the bank works with more than 12,000 loan contracts and it would take several years to analyze them manually. Now Chase is working to find ways to further apply this data – for example, to train the system to search for patterns and make assumptions based on them.

Bank of America

The chatbot from this bank is a real financial consultant and strategist. The system analyzes user data and warns in cases where the client has showed slightly different buying habits and reminds him of the need to pay his bills. Bank of America’s chatbot also knows how to perform simple operations with bank cards, such as blocking and unblocking cards.

Wells Fargo

This bank has developed a smart chatbot to turn interaction with the site into a simple and convenient procedure. Wells Fargo bank developed the Predictive Banking analytics system, which is able to notify customers about unusual situations; for example, if the client has spent more than the average amount of his checks. The system may also offer to save a certain amount on a deposit if the client received a money transfer that is larger than the amount of money he usually keeps in his account.

Citibank

Citibank has developed a powerful fraud prevention system that tracks abnormalities in user behavior. In particular, the system is polished to detect fraudulent credit card transactions when shopping on the Internet.

US Bank

This bank has developed the Expense Wizard, an application that allows clients to manage their accounts as well as book airline tickets and accommodations abroad. This app focuses on secure payments in other countries. It is very convenient for those who go on a business trip without a corporate credit card, since the application allows the user to collect all financial data about the trip in one place and create a report for his company’s financial department.

PNC

This bank holding company and financial services corporation invested $1.2 billion from 2016 to 2021 in Machine Learning, with a goal to obtain quicker, safer, and more stable services and operations. The company bet on an internal cloud environment, making the best of AI and ML. PNC joined forces with an AI vendor named Anaconda for this project to renew their data science infrastructure and adapt it for R and Python. This move resulted in PNC being able to build in-house Machine Learning models and, in addition to that, migrate the PNC’s infrastructure into Anaconda Enterprise 5.2.

Bank of NY Mellon Corp

One of the other inspiring Machine Learning use cases in banking comes from an organization with over 200 years of history in the industry. They bet on robotic process automation (RPA) to save on costs and boost the efficiency of operations. You could make the argument that RPA is not Artificial Intelligence or Machine Learning and you would be correct. However, RPA integrates with Artificial Intelligence, and some processes are run by software “bots”, not actual mechanical robots.

Four years ago Bank of NY Mellon Corp launched nearly two hundred bots to handle various tasks automatically, such as requesting data from external auditors, transferring funds, and fixing formatting and other data mistakes. As a result of the integration of RPA, the organization managed to receive a 100% accuracy of validations in account-closures across five different systems. The processing time has improved by nearly 90%, while trade turnaround time was improved by almost 70%.

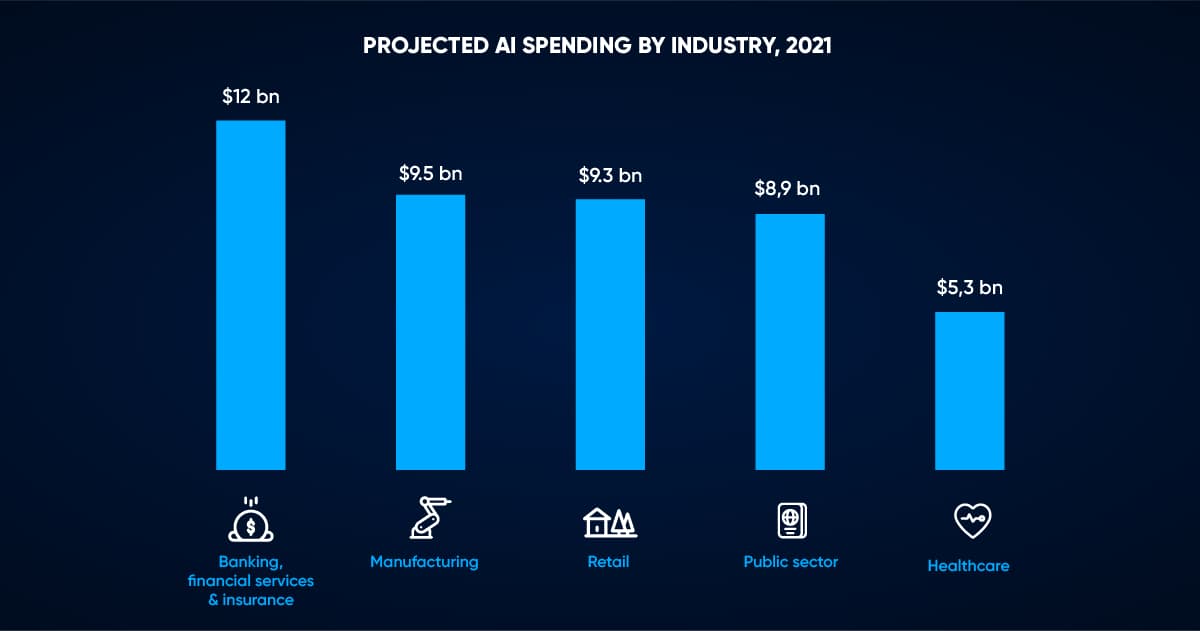

Application of Machine Learning in Banking will expand in 2021

Why? Because the Banking, Financial Services and Insurance industries are already expecting around $12 Billion in investments this year, far exceeding other industries. Despite the Covid-19 pandemic, Artificial Intelligence and Machine Learning in the Banking sector will boom, just as projected before the unfortunate events. Take a look at this infographic with the most recent predictions:

Are There Any Risks in Adopting Machine Learning for Banking?

Of course, Artificial Intelligence technology can revolutionize the banking sector. However, there are certain risks — but they are mostly associated with the novelty of technologies and the lack of full understanding among users about how they really work.

Job Cuts

This is one of the most common risks and fears associated with AI and machine learning, even regardless of their scope of application. However, modern research suggests that Artificial Intelligence in the banking sector will provide a much larger number of new jobs compared to the number of professions that will become unclaimed. Also, do you remember the study we talked about at the beginning of this article? Sixty percent of AI talents are hired by financial institutions. This already gives sufficient reason to say we should not expect a total collapse.

Less Trust Due to Less Human Contact

There is also an opinion that users will feel less confidence in financial institutions because of fewer opportunities to work with human consultants. This is true, but only partially. Most likely we will observe this trend, but only in relation to people born in the previous generation, who are not too inclined to believe in technology to begin with. But as for the generation of millennials who are willing to pay more for convenience and reliability, they will be glad for the opportunity to perform any operation in a few clicks.

Ethical Risks

Ethical risks are associated with the fact that the amount of data financial companies collect, store, systematize, analyze, and use to their advantage (as well as to the benefit of customers) continues to grow. Some users do not like this trend, but at the moment it is impossible to take any action without leaving a trace of personal data. Fraudsters most of all do not like this fact, since they are already beginning to feel it is becoming harder and harder to trick AI systems. At the same time, this is a definite plus for improving the user experience and enhancing the level of security.

False-Positive Results Risks

Machine learning systems and AI track patterns of user behavior and compare them with accepted versions of the norm in relation to each user. So, for example, if a user completes a transaction abroad, but he has not notified the bank about his trip (or the bank for some reason could not catch this information; for example, the user did not buy the ticket from his credit card, but received it as a gift), then this operation can be interpreted as fraudulent. But in fact, everything was legal – just a small lack of information led to a false-positive result.

How to Choose the Best Partner to Develop Machine Learning Solutions for Your Financial Service

By introducing AI into their business processes, financial organizations should clearly understand their goals — because simply analyzing data is not the ultimate goal; AI is a way to help achieve a specific goal. Therefore, when developing an AI and ML solution for a bank or another financial company, you need to make sure that the company you entrust this task with understands the specifics of your business and is aware of what tasks this software should complete.

In addition, when choosing a potential AI vendor, make sure the company already has experience in developing solutions specifically for the financial sector. Why? Because the security requirements are higher than in any other field, perhaps only with the exception of healthcare.

Conclusion

Artificial Intelligence and Machine Learning in the financial sector can make these organizations more profitable and increase client trust. However, for this to happen, your AI solution must be developed by a competent team of specialists. In this regard, SPD Technology has experience in not only providing Web development services and mobile app development services to financial institutions but also in developing Machine Learning and Artificial Intelligence solutions for the Financial Services industries.

Further Reading

- Wire transfer fraud

- Fraud Detection in the Banking Industry and the Significance of Machine Learning

- AI-Based Fraud Detection in Banking – Current Applications and Trends

- Facts + Statistics: Identity theft and cybercrime

- Mortgage Fraud

- Podcast: How banks detect money laundering

- Anatomy Of A Bank Fraud

- Counterfeit currency and security documents

- Counterfeit fraud – tips, tools and techniques

Ready to speed up your Software Development?

Explore the solutions we offer to see how we can assist you!

Schedule a Call